Buy the Company of your Choosing…

What Is Stock?

What Is Stock?

Most people know something about the stock market, but many investors who see stock as a way to get rich quick might not understand exactly what stock is and how it works. Before jumping feet-first into investing in stocks, it is important to understand some of the basics and the risks involved in owning stocks.

A company can raise money by “going public” and selling a portion of the company by issuing stock; this is called equity financing. The advantage to the company is that it doesn’t have to pay back the money or pay interest right away, as it would to a bank if it borrowed the money it needed. The advantage to the shareholder is the potential to make money through dividends and/or capital appreciation.

Dividends are taxable payments to shareholders from the company’s earnings. They are generally paid quarterly in cash, but there is no guarantee that dividends will continue to be paid. Capital appreciation is the difference between the amount paid for a stock and its current value. Shareholders also have the ability to trade their stocks on an exchange at any time.

Stock is quite simply a share in the ownership of a company, which is why stockholders are called shareholders. When you buy stock, you are actually buying a piece of the company it represents; you have a claim on part of the corporation’s assets and earnings.

As a partial owner of the company, you therefore take on the potential risks and benefits of that position, but you don’t have to put any effort into running it. Your ownership is determined by the number of shares you own divided by the total number of shares sold by the company. For example, if a company has issued 1,000 shares and you have 10, you own 1 percent of the company. Of course, if you own 10 shares of a large company that has issued millions of shares, your equity in the company is quite small.

If a company is profitable, it may decide to pay dividends to shareholders from its earnings. On the other hand, some companies may decide to reinvest profits back into their businesses rather than pay dividends. Investors have the potential to make money from dividends as well as from appreciation in the value of stock shares on the open market. Thus, stockholders have the potential to make money if the company does well and the potential to lose money if the company does poorly. The return and principal value of stocks fluctuate with changes in market conditions. Shares, when sold, may be worth more or less than their original cost.

Shareholders of common stock often have voting rights on major issues at annual meetings, usually electing a board of directors. In this way, shareholders have a say in the way the company is run. Owners of preferred stock usually don’t have voting rights but have a higher claim on the company’s assets and earnings than common stockholders do. If a company pays dividends, preferred stockholders receive theirs before common stockholders.

There is always a risk when investing in stocks. Generally, the greater the risk, the greater the potential reward. You should determine your risk tolerance and financial goals before deciding to invest in stock investments.

The information in this article is not intended to be tax or legal advice, and it may not be relied on for the purpose of avoiding any federal tax penalties. You are encouraged to seek tax or legal advice from an independent professional advisor. The content is derived from sources believed to be accurate. Neither the information presented nor any opinion expressed constitutes a solicitation for the purchase or sale of any security. This material was written and prepared by Emerald. © 2014 Emerald Connect, LLC

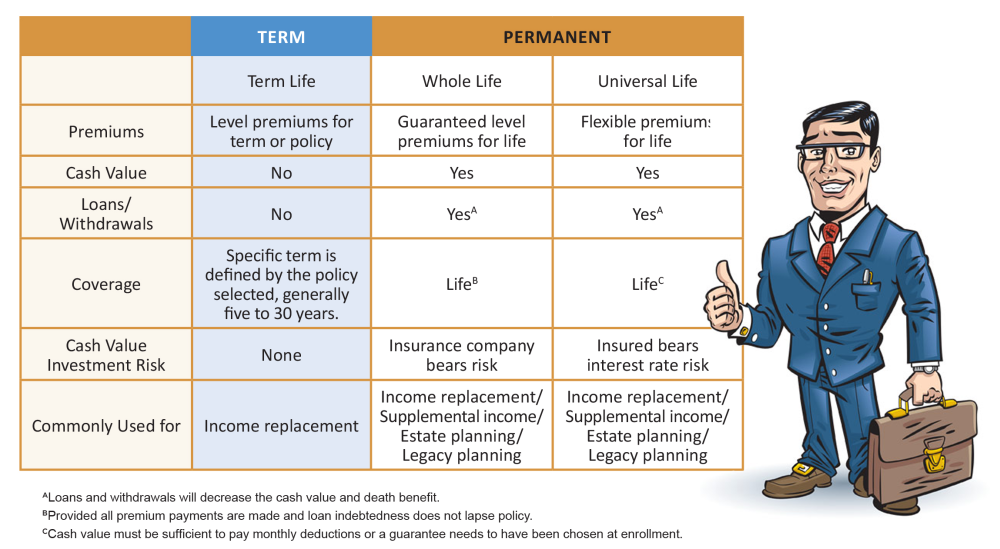

What Are the Basic Types of Life Insurance?

What Are the Basic Types of Life Insurance? What Is Universal Life Insurance?

What Is Universal Life Insurance?